SHORT: Medpace (NASDAQ: MEDP)

Peak GLP-1 Tailwinds Reversing as Trial Demand and Pricing Normalize

Summary:

Medpace is a CRO primarily focused on serving small to mid-staged biopharma companies through phase I-IV drug and medical device development services. The stock is up ~60% since pre-Q2 2025 and and has been through a lot over the past year:

Up ~55% post Q2 2025 earnings on new business growth coming in ~18% higher than the street, net revenue was also ~12% higher than the street; consensus caught offside as many expected a negative quarter

Up another ~9% on the Q3 2025 print as the book-to-bill ratio improved to 1.2x vs 0.96x in H1 2025

When the company reported Q4 2025 results in February, the stock dropped ~16% as book-to-bill came in at 1.04x vs. 1.15x, as bookings missed based off elevated booking cancellations in the quarter

It trades at ~23x EBITDA vs. comparable CROs at ~11.0x. Medpace has had stronger growth relative to comps and this is primarily due to Metabolic having grown at a 45% CAGR since 2022. The evidence I’ve gathered suggests that they’ve benefitted from the hype that piled into weight loss and obesity drugs by newer incumbents over the past few years. I seen an opportunity as there are multiple signals that trials are being cancelled, and that the broader weight loss industry is starting to reverse from a supply-constrained, high pricing-power environment into a buyers market with pricing pressure, which should further slow TAM for new entrants and therefore demand for these trials. There are 5 main things here:

Industry Pricing in Structural Decline Should Reduce TAM: Increased competition as supply normalizes, DTC mix shift, MFN pressures from the Trump admin, and increased rebate demand from insurers are compressing prices across weight loss drugs, making unit economics less attractive and lowering TAM for new entrants

Semaglutide Exclusivity Eroding Incentive for New Entrants: Semaglutide loses exclusivity across major markets this year and generics should emerge, reference pricing across the obesity space should fall, further weakening the economics and TAM / incentive for new entrants

Slower Funding Conditions: Funding conditions for early-stage biopharma softened in 2025, I calculate there to be a 12-15 month lag between fundraising and when these players look to kick-off trials, implying that the weaker backdrop over the past year should translate into decreased trial starts

Trial Cancellations Appear to be Continuing Through 2026: ClinicalTrials.gov data suggest cancellations have continued in 2026, using this as a readthrough implies that this year should be weaker

Obesity Trials are Getting Longer and Harder to Run: Competitor websites state rising troubles with executing weight loss trials due to heightened placebo awareness which has led to lower patient retention rates, making trials slower, more expensive, and less attractive for small and mid-sized sponsors

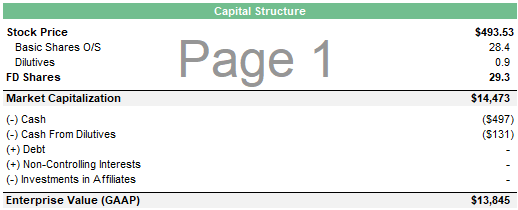

I believe the multiple should contract back down to pre-“GLP-1” levels as growth decelerates. Assuming this contraction and a 25% slowdown in obesity trials implies >20% IRR with ~2.0x R/R. Short is actionable as Medpace is a ~$14bn market cap name and liquid.

The Business:

Medpace was founded in 1992 by August Troendle (current CEO and Chairman) and operates as a Contract Research Organization (“CRO”). For context, CRO manages clinical trials for drug developers and biotech companies to determine the effectiveness and safety behind new drugs. This business exists because biotech companies typically don’t have the necessary infrastructure, teams, or compliance with regulatory oversight to run these often long and costly R&D processes themselves, they engage CROs to handle the “heavy lifting” of these trials.

Execution of these trials can include processes like recruiting patients, managing doctors, analyzing data, and handling the regulatory submissions.

The revenue here comprises of service fees for these clinical trials, which vary per contract and are primarily based on the scope of work and complexity. Pricing for these contracts usually come in two forms, fixed fee (most common), and fees paid for specific activities completed.

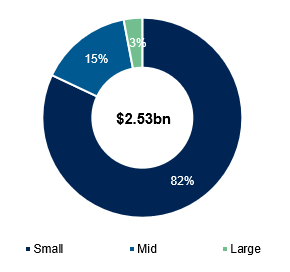

What Medpace focuses on vs other CROs comes down to the CRO model and clientele. Medpace focuses primarily on the full-service outsourcing model (FSO) versus larger peers that are mostly functional service providers (FSP), the main difference is that the FSO model typically owns the entire process behind the trial (study design, patient recruitment, monitoring, regulatory work, etc.), whereas the FSP model focuses on specific parts of a trial (i.e. data management, biostats, etc.). The FSO model naturally results in higher revenues per trial, but is mainly used to service small/mid sized sponsors as opposed to larger biopharma players that tend to have greater capabilities in the R&D process. This is the case for Medpace, which focuses on Phase I-IV trials and has a customer base comprising 82% and 15% of small and mid-sized biopharma sponsors as of 2025 respectively.

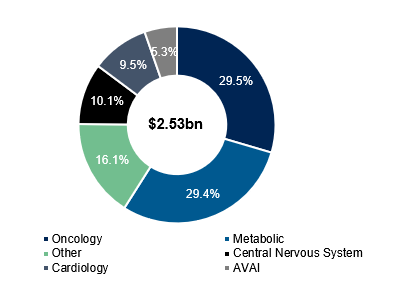

Medpace has the most exposure to oncology and metabolic end-markets, but oncology has historically been the bread and butter of the business:

FSO players: Medpace, Fortrea, ICON (in certain programs)

FSP players: IQVIA, Thermo Fisher, ICON

Most CROs tend to operate in a fix between the two models, but Medpace crowds around FSO.

Context Around The Weight Loss Drug Industry

To understand the short here, understanding what supply / demand dynamics have looked like in the weightloss industry is also useful to contextualize, a high-level timeline can be summarized as follows:

(2017 - 2022) Incretin-Based Therapy Moves From Diabetes to Obesity:

Earlier-generation “GLP-1s” including liraglutide (Novo) and dulaglutide (Lilly) used in diabetes treatment provide initial proof-of-concept for pharmacological weight loss, but with modest efficacy (~5–8%) and limited commercial uptake

FDA approves semaglutide-based Ozempic (Novo) in late 2017 for the treatment of type 2 diabetes, clinical trials revealed significant weightloss as a consistent secondary outcome

Narrative around obesity / weightloss in the pharma industry starts to shift from lifestyle condition to chronic metabolic illness requiring pharmalogical management

Wegovy (also Novo) becomes FDA approved in 2021 and is introduced as a high-efficacy purpose built obesity therapy, established a new commercial and clinical benchmark

Lilly advances tirzepatide (Mounjaro), a dual GLP-1/GIP agonist and introduces next wave of efficacy step-change

(2022 – 2023) Efficacy Step-Change Drives Demand Shock:

Launch and scale of Wegovy and Mounjaro (and later tirzepatide-based Zepbound) reset efficacy benchmarks (~15–20%+ weight loss), driving sharp demand surge

Widespread shortages of “GLP-1s” as supply lags demand

Four GLP-1 drugs (tirzepatide, semaglutide, dulaglutide, liraglutide) added to FDA’s shortage list, allowing for compounding to temporarily fill part of the supply gap (compounders mostly focused on tirzepatide and semaglutide)

Significant capital inflow into obesity across large pharma and biotech

(2023 – 2025) Supply Constraints + Rising Barriers:

Compounding continues through 2024

Clinical benchmarks continue to rise, compressing differentiation for new entrants

FDA declares the shortage of semaglutide and tirzepatide resolved, begins crackdown on compounding to continue into 2026

Novo and Lilly start focusing on delivery over efficacy (oral vs. injectable) more than before

Short Rationale

The Set-Up:

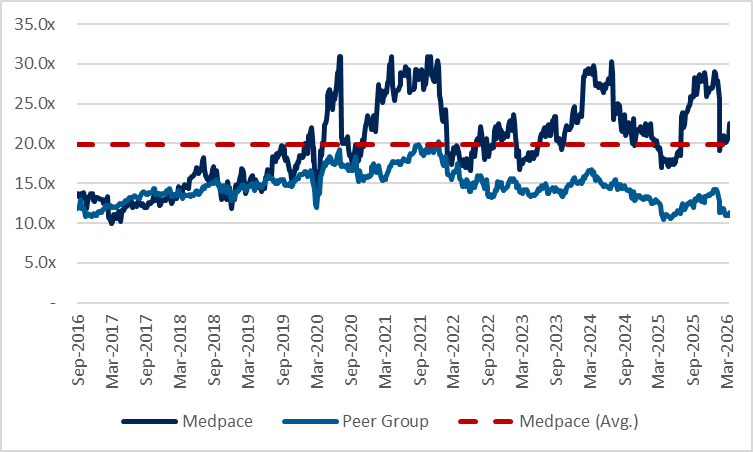

Medpace has materially outperformed the broader CRO group over the past few years, up ~130% since 2022 versus comparable CROs that are down ~40%…

…at the same time, the multiple has expanded from ~18x to ~23x with the stock trading at a meaningful gap over comps at an average of 10-12x despite similar margin profiles across the industry. The outperformance here reflects stronger bookings growth coming from greater exposure to end markets that have been favorable over the past 2 years...

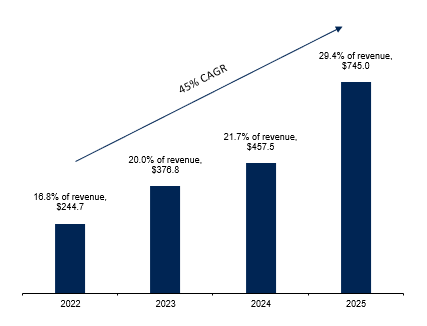

…most of this is coming from metabolic, which has grown at a 45% CAGR since 2022. but digging further, I believe the growth in metabolic has a lot to do with weight loss drugs, since the hype around “GLP-1s” started around that time.

Prior to mid-2025, smaller biopharmas (>80% of Medpace’s clientele) chased the hype around obesity / weightloss drugs in light of a few catalysts, but primarily being driven by:

Breakthrough clinical efficacies, with real inflection coming from GLP-1/GIP combinations developed by Lilly, and an arms race to find the next big thing

Persistent undersupply of branded GLP-1s and other name brand obesity drugs (which the FDA also attempted to temporarily be addressed through compounding)

Metabolic studies take much less upfront capital and time to complete - can get a metabolic study down within a year compared to oncology which takes multiple years

Confidence from sponsors - oncology is naturally riskier given complexity and length of trials

Medpace doesn’t say too much about how growth was tied to weight loss, but they sort of confirm the rise in these trials in external articles / videos:

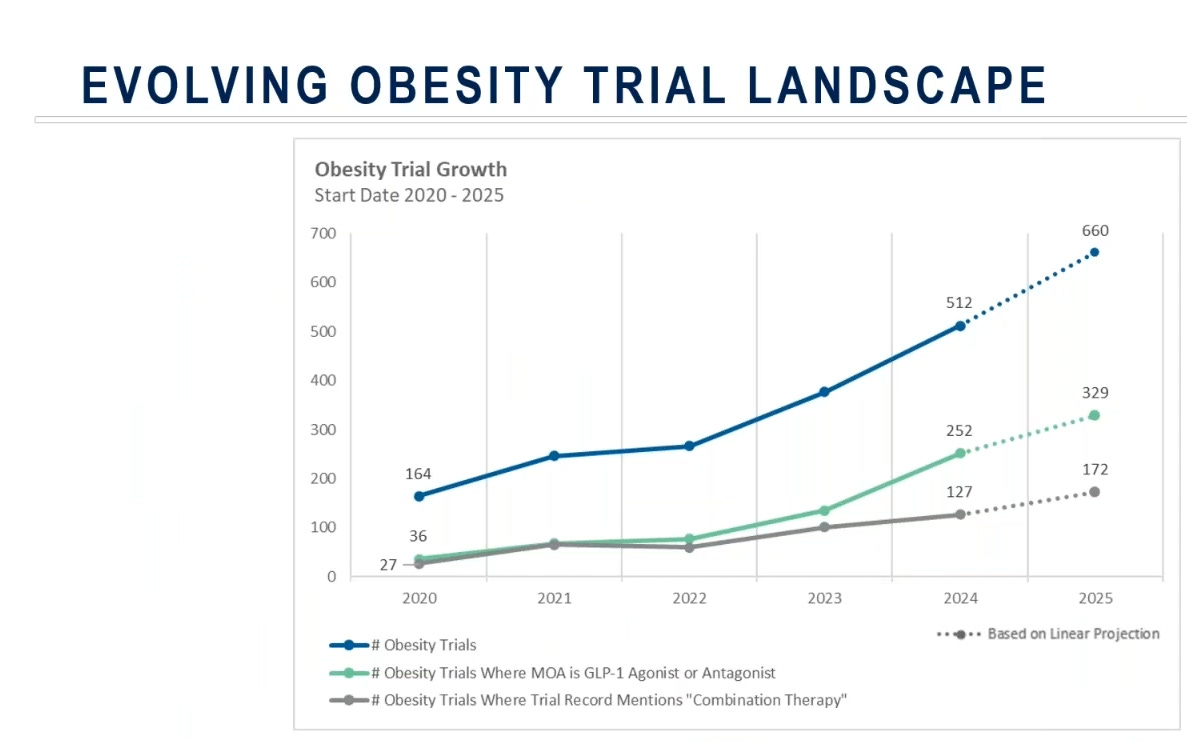

“There has also been a sharp rise in obesity-related clinical research, from 164 trials in 2020 to over 500 by 2024, with GLP-1 mechanisms representing roughly half of new studies. Combination therapy designs expanded fivefold, signaling a clear pivot toward multi-agent strategies.”

(Source)

(Source)

It’s also worth noting that the CEO / Founder August Troendle and President Jesse Geiger both come from a metabolic background and are noted to be very well connected, which might explain part of why they were able to capitalize on the tailwinds here. Medpace’s metabolic segment today earns as close to as much in revenue as their oncology segment...

…but Q4 hinted that the trend is starting to unwind.

Summary of how the stock has traded over the last 3 earnings:

54.7% – July 21, 2025 – Q2 2025

Biggest item was surprising on bookings growth – everyone was caught offside, as checks indicated soft biotech funding environment; overall, most people were likely net short / bias short coming into the print

Net new business came in 17.8% higher than the street, and net revenue came in 11.8% higher than the street – book-to-bill came in at 1.03x vs 0.98x

Upside was largely attributable to lower cancellation levels vs. recent Qs in addition to therapeutic mix shift (metabolic) towards faster burning trials

9.1% – October 22, 2025 – Q3 2025

Book to bill improved to 1.20x vs 0.96x in H1 – cancellations rates inline with expectations, and mostly in line with exceptions

Management beat and raise across revenue, etc., but major focus was book to bill improving and backlog growing

(15.9%) - February 9, 2026 - Q4 2025

Despite strong revenue and earnings, stock was down as bookings missed significantly, down 7% sequentially over Q3 2025 – net book-to-bill ratio came in at 1.04x vs. 1.15x

Net bookings miss was result of broad-based elevated bookings cancellations in quarter, which reached highest level in a year

Management stated cancellations to related to funding challenges but skewed towards metabolic trials, a therapeutic area management expects to decline as % of total mix

Management guidance assumes that cancellation rates normalize

The most notable thing is here is that Q4 started to challenge the growth narrative since despite solid headline revenue, bookings fell short and management lightly noted that they experienced a step-up in cancellations partly skewed to metabolic trials, as well as growth in that segment to normalize:

“Cancellations were a little bit skewed towards metabolic area that’s been growing quite a bit. So there were a higher level of cancellations there. Overall bookings have continued to be oncology our strongest. Metabolic still there, but there were some elevated cancellations.”

(Source)

“...metabolic will be decreasing as a percent of our revenue next year, I think. So I think it’s going to kind of somewhat normalize, head towards more normal range, but I don’t really see that as a big risk for us at this time.”

(Source)

“So yes, to August comments, we do expect some of that metabolic shift to slow down a little bit. I wouldn’t say it’s materially so, but we do expect it to slow down a little bit.” (Source)

Many on the sellside are viewing these cancellations as transient and temporary…

“The only real incremental update we got was that cancellations ticked up materially in 4Q and caused the bookings miss. With plenty of questions around what caused this, we think a part of the elevated cancellations could be due to some mean reversion as cancellations had been below typical average in 2Q and 3Q.”

- Barclays (Feb 10, 2026)

…but I believe these cancellations are structural, driven by supply catching up to demand after a period of tight supply and elevated pricing, with smaller biopharmas now easing out of chasing the success of Ozempic and related obesity-drugs. Medpace trades at at 23x vs. ~18x pre weight loss era, so I suspect there is room for this to fall.

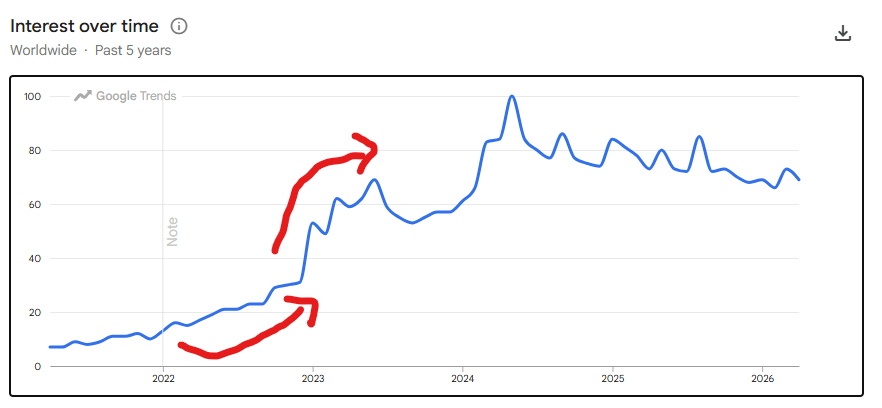

One funny observation is that Medpace’s share price chart looks similar to how Ozempic search interest looks over the past 5 years, both starting to pick up in 2023.

Quantifying Exposure

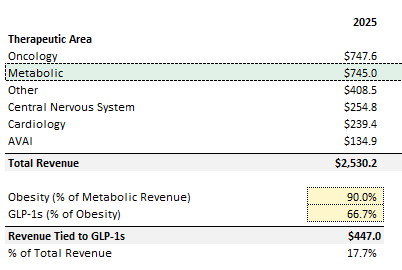

I pieced together high-level disclosures and commentary that management provided in past earnings calls to determine how much of today’s revenue is tied to obesity. Management notes that metabolic is concentrated around obesity (without exact numbers), but they also mention 2/3rds of obesity is related to “GLP-1s” (source). Assuming 90% of metabolic is obesity (with the remainder tied to diabetes / NASH), this would imply ~18% of Medpace’s revenue is tied to the broader GLP-1 category:

Why Is This Being Overlooked and Why Now?

Most of the sell-side analysts covering this name don’t cover GLP-1 exposed names (NOVO and LLY):

Justin Bowers from DB – no

David Windley from Jefferies - no

Sean Dodge from BMO – no

Rachel Elfman from Morningstar – no

Jamie Clark from Rothschild Redburn – no

Dan Leonard from UBS – no

Jailendra Singh from Truist – no

Eric Coldwell from Baird – no

Max Smock from William Blair – no

Michael Cherny from Leerink Partners – yes, covers Hims and Hers

Ann Hynes from Mizuho – yes (covers a lot of major HC companies so should be plugged in)

Charles Rhyee from Cowen – no

Luke Sergott from Barclays – no

So out of the 13 analysts, only 2 cover other names which indicates they should know about this.

The key variable for how this trades over the next few quarters is what book-to-bill ends up looking like. My view is that book-to-bill will weaken as trial demand slows, and this is being driven by TAM of the weightloss drug category being written down to reflect lower pricing. This should reduce incentive for new entrants and lead to continued cancellations. There are a few signals that show the cycle is reversing:

Structural Industry Price Compression Reducing TAM and Incentive for New Entrants

Loss of Semaglutide Exclusivity

Weakening VC Funding Backdrop

Clinicaltrials.gov Data and Industry Participant Anecdotes

Obesity Trials Are Becoming Increasingly Difficult to Execute

1. Structural Industry Price Compression Reducing TAM and Incentive for New Entrants

2023 - 2024 was defined by a massive pricing umbrella created by high listing and cash prices given shortages at the Novo / Lilly duopoly, the market is now shifting from scarcity pricing to price compression.

Why does this matter for Medpace? Pricing compression of the market leading drugs (semaglutide being the most notable) results in structural compression across all drugs in the industry. The original investment case for smaller and mid-sized biopharmas entering the space depended on strong ROI and an expanding TAM with high realized prices, not just volume growth. And so this reduces the economic justification for new entrants, meaning the growth story over the past 2+ years is at risk.

There are multiple avenues of existing and future price compression, but I believe the main 4 are i) competition, ii) increase of DTC sales channel, iii) MFN pressures from the Trump admin, and iv) increased rebate demand from insurers

Lilly notes that pricing headwinds are structural across the industry…

“Pricing, I would say, both U.S. and OUS. is certainly one of those things that are basically a headwind to the industry as a whole. I don’t think that is just individual for the incretin space, but it’s to the entire pharma industry.” (Source)

…and guides to low to mid-teens pricing compression

“We expect to deliver industry-leading volume growth driven by our key products, partially offset by lower realized prices. Price is expected to be a drag on growth in the low to mid-teens.” (Source)

Novo explicitly guides to a 5%-13% YoY decrease in revenue despite volume growth…

“In terms of outlook for the year, we’re guiding between minus 5% and minus 13% on the top line. It’s driven by some certain extraordinary effects, including LOE in international operations in specific markets, impact from MFN in the U.S. as well as declining prices, mainly in the U.S. linked to a higher proportion of cash business as well as rate enhancements on the insured side. Of course, we continue to drive volume, and we are looking into volume growth and more patients being on Novo products in 2026. However, the price effect outweighs that.” (Source)

…and stated they will cut U.S. list prices for WeGovy and Ozempic by up to 50% and 35% respectively starting in Jan 2027.

What will exacerbate price compression across the broader industry is that much of it relies on the DTC channel, where biopharmas are already realizing lower cash-pay prices. As DTC continues to grow, more patients are bypassing list-price-based reimbursement and buying at cash prices, which are typically more elastic and lower, putting further downward pressure on pricing for the broader market and impacting incentive for new entrants:

(Source)

A Reuters article provides a great overview on this price war and puts into context how both cash and list prices will change over the near-term (Source):

Novo slashed cash prices to a range of $149 to $499 a month (depending on drug and dosage)

Meanwhile, Lilly is selling Zepbound at cash prices ranging from $299 to $449, discounted off a list price of more than $1,000 a month.

Jan 2027 effective date of Novo Nordisk’s list-price cuts will coincide with new and lower prices for the same drugs in the federal Medicare health-insurance program for the elderly

Medicare prices for Ozempic and Wegovy starting in January 2027 will be $274 for a 30-day supply. The Medicare prices resulted from negotiations last year between the Medicare agency and Novo Nordisk

Government pressure on weight loss drug pricing has also intensified significantly under pressure from the Trump admin to match lower prices found in other developed nations (most favoured nation) pricing: (Source)

MFN semaglutide drugs cut to a list price of $675/month, representing a 50% decrease in price for Wegovy and a 35%

Novo also agreed to list semaglutide drugs on the TrumpRx website for an even greater discount (priced at $350

Zepbound and Orforglipron (if approved) priced at at an average of $346 on TrumpRx down from $1,086 per month

Wegovy pill and other oral “GLP-1” drugs in the pipeline priced at $150

Beyond political pressure, U.S. insurers are demanding higher rebates, further reducing the “realized price” Novo actually receives for each sale, or forcing them to cut prices to be covered

Only 36% of employers and 22% of plans currently cover the drugs for obesity. About 7% of these companies are considering stopping coverage (Source)

Using this as a read through for the rest of the industry, small biopharma companies in the metabolic space may be cancelling their trials as they don’t see a profitable way to capture TAM in the market / be included in insurer plans

Another Reuters article from February 2nd confirms the sentiment that TAM is shrinking in the obesity market: (Source)

“The long-held Wall Street expectation that the global market for obesity drugs would reach $150 billion in the next decade is looking a lot less certain with U.S. prices falling for GLP-1 treatments from Novo Nordisk (NOVOb.CO), opens new tab and Eli Lilly (LLY.N), opens new tab and competition heating up in the cash-pay consumer market”

“Unprecedented demand for the potent new weight-loss drugs targeting the GLP-1 hormone led analysts to project a market of $150 billion - or even $200 billion - by the early 2030s. But 2030 forecasts are around 30% lower at about $100 billion or so and that $150 billion target has shifted to 2035 for some.”

“’That $150 billion pie is gone, even if you’re very bullish on volumes,’ said Jefferies analyst Michael Leuchten.”

“Goldman Sachs analysts also pared back expectations. Their current estimate for global obesity drug sales by 2030 is $105 billion, down from earlier forecasts of $130 billion, based on steeper price erosion and changing customer-use patterns.”

2. Loss of Semaglutide Exclusivity

TAM compression should also happen as weight loss drugs are becoming actively commoditized. A wave of cheaper, “good enough” drugs will hit major markets this year, which will expand supply and reset the pricing that new entrants can reasonably command.

The main thing here relates to Novo and Semaglutide. Semaglutide owns >30% of the weight loss market share being the active ingredient in Ozempic and Wegovy, and plays a major role in effectively setting the reference price for the entire weight loss drug category. While it is an older and less effective drug than newer GLP-1/GIP combinations, the key point to note is that Semaglutide is effective on an absolute basis, which limits the willingness of patients to pay a meaningful premium to limited incremental efficacy, especially considering the main barrier to patients using these drugs in the first place primarily came down to price:

“The biggest barrier to taking Ozempic is not side effects or worries about its efficacy but its cost. When you’re talking about two, three, four hundred dollars a month, for a lot of people, that is just impossible.”

(Source)

Many users of this drug also describe it as good enough:

Novo owned the patent on Semaglutide which kept the prices of the drug high prior to active competition from Lilly and everything mentioned prior. Those patents are now half way through expiry in the US (expected end of 2031) and are set to lose exclusivity this year in major geographies including Canada (already expired), India, China, Brazil, Turkey, which make up ~33% of global obese adults population. Generics should come to market this year for semaglutide, at a discounted cost, shrinking the TAM and entry incentive for small / mid-sized players further.

The following articles reported the following on what Canadian / Indian generics could look like in terms of pricing, implying significant compression to current levels:

“As of January 2026, Health Canada is reviewing nine submissions for generic semaglutide from companies”

“Some manufacturers have suggested generic semaglutide prices could be 60 to 70% lower than branded versions, potentially as low as $60 to 70 per month in some scenarios.”

(Source)

“Meanwhile, in India, several companies obtained early approval for generic replacements and began selling them the day the patents expired. One Indian company was offering generics for as little as C$19 a month. Analysts expect around 50 generics could enter the Indian market within months.”

(Source)

gain, semaglutide is good enough for most people and generics should exacerbate this TAM and incentive shrinkage through increased competition, as well as adding onto the pricing pressures mentioned prior.

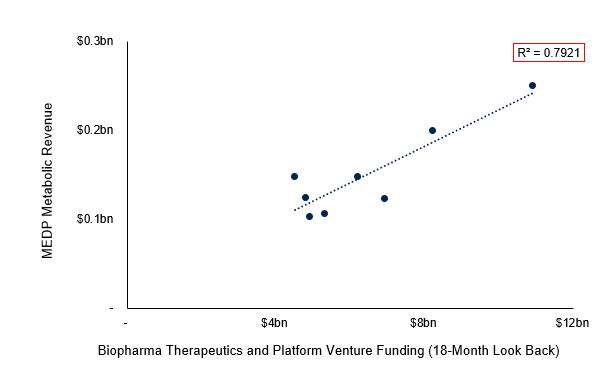

3. Weakening VC Funding Backdrop

The softer funding environment (relative in comparison to prior years) in 2025 and early 2026 should impact what trial starts look like in 2026.

Historical industry benchmarks suggest that there’s a delay between the time that a small to mid-sized biopharma raises capital to when they kick off Phase I trials. Based on a report from PPD (Thermo Fisher’s CRO, source), I assume that there’s a 6-10 month delay in lieu of start-up times. Considering both these factors, this would imply that the book-to-bill that Medpace reports in the upcoming quarters would be variable to the funding backdrop in 2025 and early potentially early 2026.

A regression between Medpace’s quarterly metabolic revenue from 2024 and 2025, and total biopharma VC funding (used as an approximation given lack of data on funding for weightloss bipharma specifically) based on an 18-months look-back yields a fair bit of significance.

This is something that was also echoed via echoed on Tegus expert calls:

With this relationship in mind, using total biopharma funding as a lookthrough at how small to mid sized weightloss has performed, IQVIA’s most recent R&D trends report notes that biopharma funding took a ~20% hit from 2024 to 2025, with the amount raised in IPOs also reaching 5-year lows:

Data from JPM points to in the same direction, VC biopharma investments decreased ~12% YoY in 2025. Fewer companies completed venture financings, but those that did were increasingly later-stage and larger in size, which means investors are instead chasing more scaled opportunities rather than smaller players that are actively initiating new programs.

(Source)

The weaker biopharma funding that was took place over the past few quarters should result in lower demand for trials in these upcoming ones.

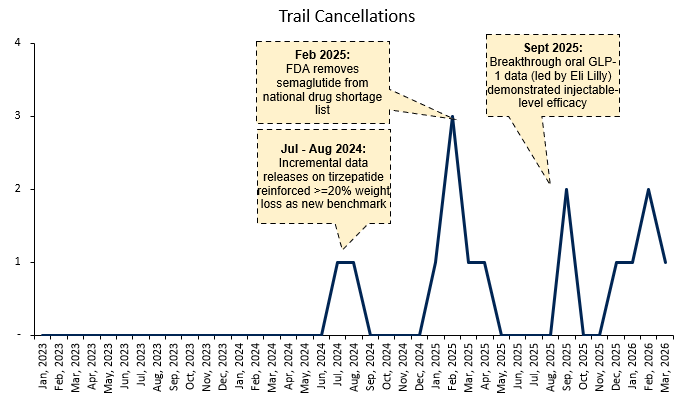

4. Clinicaltrials.gov Data

This is meant be used moreso as a readthrough (given the data is imperfect), but based on clinicaltrials.gov data, trial cancellations have inflected since December and early into 2026. The data shows that this has previously tended to happen around news where it would imply that the addressable market for smaller and mid-sized players are being compressed.

Two examples stand out:

Cancellations increased in Jul - Aug 2024, coinciding with incremental tirzepatide (Lilly’s drug) data that reinforced >20% weight loss as the new efficacy benchmark. This likely had the effect of rendering a large portion of existing pipelines economically non-viable, as programs targeting lower efficacy thresholds would struggle to compete on both relevance and pricing power

Another spike happened in September 2025 following breakthrough oral GLP-1 data from Lilly demonstrating injectable-like efficacy. This would have been understood by smaller players as further concentrating demand toward best-in-class assets, narrowing narrows the subset of patients and use-cases they can realistically target- Q4 book-to-bill appeared very low as mentioned

A recent anecdote of this is Terns Pharma. Terns had been positioned as an emerging metabolic platform, with multiple obesity assets in development, including it’s drug TERN-601. However, by August 2025, management made a decisive strategic pivot to ceasing internal investment in metabolic and instead pursuing partnerships for this portfolio. This is a notable shift from their previous develop-and-commercialize ambition:

“The company seeks to partner our portfolio of potentially best-in-class metabolic assets and does not plan to invest in clinical development in metabolic disease beyond year end 2025.”

(Source)

After a weak Phase II readout for TERN-601 in Oct-2025, Terns went further and said it would not advance TERN-601 and reiterated that they would stop investing in other metabolic assets

“The Phase 2 topline 12-week results for TERN-601 did not meet this threshold and likely preclude further development… As we’ve previously communicated, we do not plan to further invest in metabolic disease. Our team remains energized and focused on advancing our potentially best-in-class TERN-701 program in chronic myeloid leukemia (CML) with our full capabilities.”

(Source)

The rationale for stopping investment in metabolic was cited to be the increasingly competitive landscape during Tern’s Q3 earnings, where they noted Lilly had “set the bar” in oral obesity and that Terns would need to be meaningfully better to justify continued development:

Kelly McCarthy

“Maybe let’s turn to your obesity pipeline. I think very topical, the obesity space has become quite competitive in recent years… can you share just your high-level thoughts on this space and where TERN-601 could fit in?

Amy L. Burroughs Terns Pharmaceuticals, Inc. – CEO & Director

“...we think that Lilly has really set the bar. We think as we talk to patients and physicians that there is a huge unmet need for an oral. They’re going to be the only oral GLP-1 receptor agonist like that on the market. And we think that Lilly is going to be very successful with that drug. And for us, it really sets the bar, right? Like we have to be better than that. And the bar is not as high as some people had expected.”

(Source)

What makes this interesting is that just one earnings call earlier, Terns described obesity as still early and argued that near-term oral competition was limited:

“So the obesity market is -- we actually see it as still in the early days. And although there’s a lot of competition, there aren’t a lot of oral drugs in the clinic that will have Phase 2 data in 2025. There’s a lot of sort of next-generation things that are being done preclinically that are many years behind. But in terms of oral agents that are small molecules, we don’t see quite as much competition in the near-term. And we think that ultimately, differentiation is what matters.”

(Source)

This is notable since Terns used to be one of the rising stars in the industry, and the fact they pivoted this quickly might indicate that with increasing competition and decreasing ROI, the obesity market is becoming harder for smaller players to underwrite. Merck recently announced an acquisition of Terns, and both the deal rationale and all disclosed valuation framing are entirely centered on the oncology asset (Source).

5. Obesity Trial Attrition

An emerging headwind might be that obesity trials themselves are becoming harder to execute, which has implications for existing trials and sponsor willingness to initiate new programs.

The core issue is that the traditional placebo-controlled model is breaking down. For context, A placebo is a dummy treatment with no active drug used so that researchers can isolate the true efficacy of drug (commonly required by FDA and regulators as they support whether a drug actually works). Placebo models only work if patients don’t know whether they are receiving the drug or the placebo.

What’s changed now is that “GLP-1s” are common place and widely available, so patients have an easily time determining whether they are on the active drug or placebo (an increased amount are also discussing between each other online). These patients drop out of the trials if they realize they are on the placebo (as the incentive to remain in the trial is limited), and so this has led to an increased dropout rate in weight loss trials.

“‘They see others lose 10%, 15%, 20% of their weight and nothing happens with them… so, it is clear in the studies who’s taking placebo and who is not’... consequently, CROs find themselves navigating a narrowing path. On one side sits the need for robust comparative data. On the other, a growing ethical discomfort with keeping patients on placebo for extended periods when effective therapies exist.”

(Source)

A recent article confirms this and notes declining retention for patients in these trials:

“People who don’t lose weight can quickly figure out that they were assigned to take a placebo instead of the real drug. And with highly effective obesity medications on the market - Eli Lilly & Co.’s Zepbound and Novo Nordisk A/S’s Wegovy shot and pill - that are getting cheaper, there’s little reason to stay in a study that doesn’t yield the intended benefits.”

“‘Right now, retention is challenging,’ said Barbara McGowan, a consultant in diabetes and endocrinology in London and an investigator for several obesity-drug trials.”

“‘People learn pretty quickly whether they’re on placebo or not,”’ said Raymond Stevens, chief executive officer of Structure Therapeutics Inc., which is working on an experimental pill that’s shaping up to rival new oral treatments from Lilly and Novo. ‘It’s adding a challenge to conducting clinical trials.’”

“Patients on placebo are in some cases seeking out weight-loss drugs from other sources while still enrolled in the trials… That happened with Lilly’s highly anticipated pill, orforglipron. In a large trial, 6.2% of patients in the placebo group dropped out because they weren’t satisfied with their weight loss, and 2.5% started looking for other ways to shed weight, which in some cases included different obesity medications.”

(Source)

The same article also mentions that the idea that patients are becoming more self aware through social media, which has also hurt retention:

“Go to the Reddit string on orforglipron,” said Stevens. “People aren’t supposed to be talking about these things, but it was on Reddit - during the trial.”

(Source)

Medpace’s comp Fortrea confirms this broader struggle with retention as well:

(Source)

One attempt at redesigning these trials involves comparator studies (though some regulators still generally require placebo arms). However, these increase trial complexity, duration, and cost altogether.

The net result is that obesity development is moving from relatively faster and high participation studies to slower, higher attrition, and higher cost studies which again reduces the economic viability for small/mid-sized players.

Other Observations Worth Mentioning

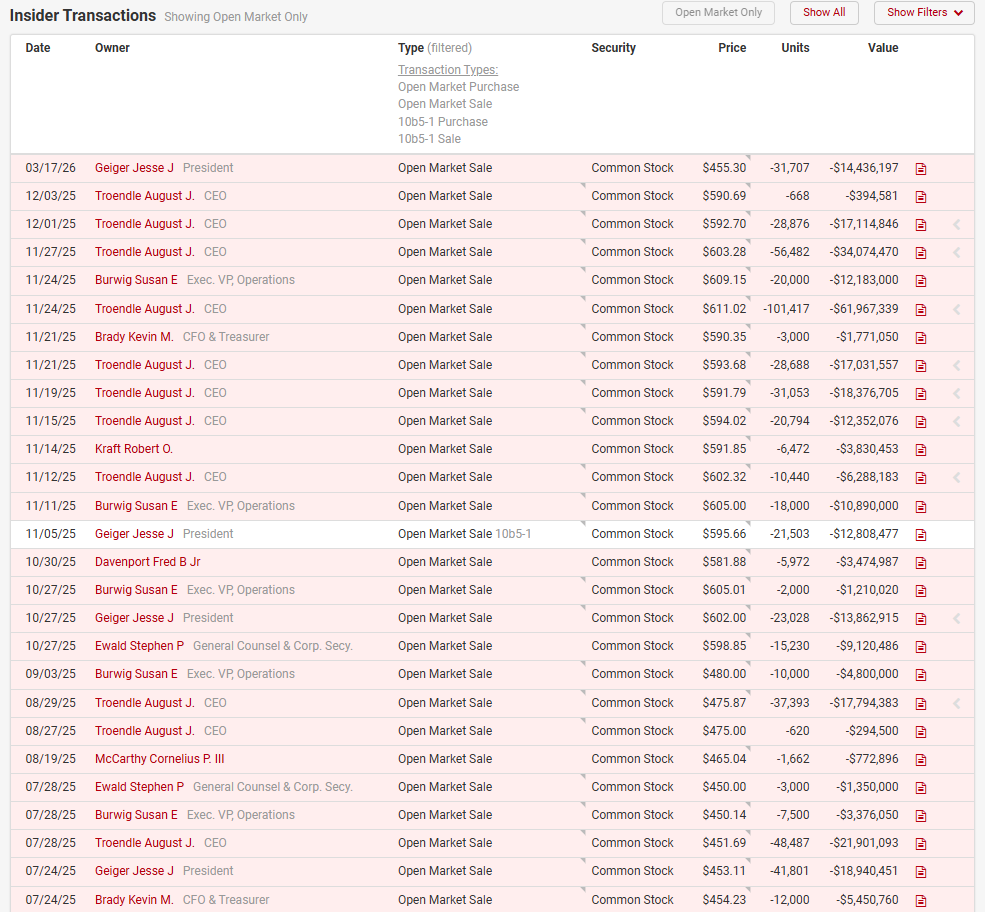

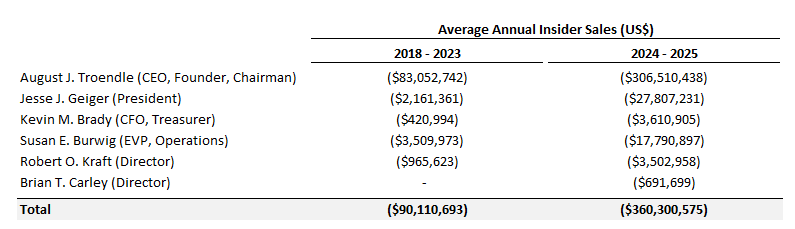

There’s been significant insider selling over the past year:

Management seems to have had a history of selling, but this has significantly ramped up over the past 2 years:

The CEO’s ownership has also decreased from ~24% in 2023 to 19% today.

Valuation

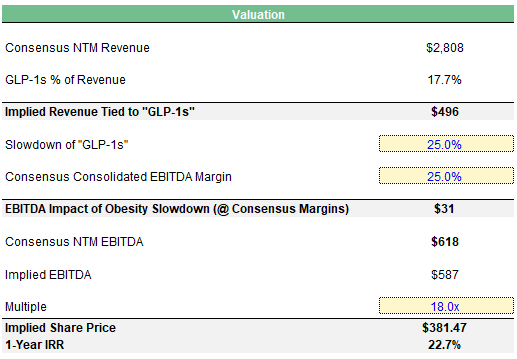

Growth should decelerate, and I believe that MEDP’s multiple can fall back down to pre-”GLP-1” levels of ~18x to reflect that. EBITDA should also be impacted from loss of trials in the process. I take a haircut to consensus NTM EBITDA estimates based on assumptions around the slowdown of obesity trials, and contribution margin from those trials.

1-Year IRR Analysis:

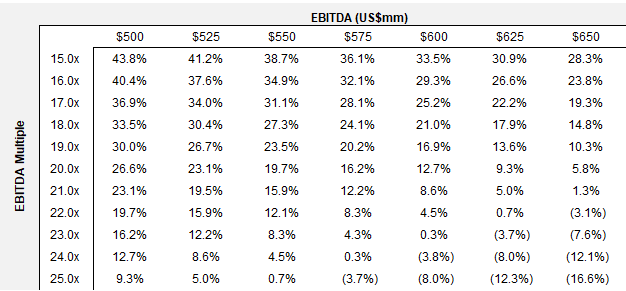

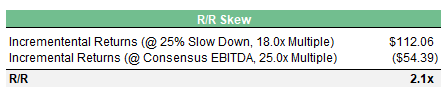

R/R under this scenario versus consensus at 25.0x is also asymmetric:

Disclaimer: This article is for informational and educational purposes only and does not constitute financial or investment advice. The views expressed are personal and subject to change without notice. This is not a recommendation to buy or sell any securities. Any reliance is at your own risk.